Rupee weakness, FIIs activity, US jobs data among key market triggers in the final week of 2025

Indian markets ended the truncated week on a subdued note, with benchmark indices achieving only modest gains amid ongoing FII selling, a weak rupee and continued uncertainty surrounding the India–U.S. trade deal. The NIFTY50 index added 0.2% for the week to end around 26,042, while SENSEX rose 0.1% to 85,041. The range-bound movement and low holiday volumes kept overall movement contained.

The broader markets also sustained the positive momentum with Midcap 150 index gaining 0.2% to 22,190 for the week and Smallcaps 250 index advancing 1.2% to 16,614. Meanwhile, the volatile index closed the week at historic lows of 9.12, down 4% for the week.

The sectoral picture was mixed, reinforcing the sense of consolidation. The Defence and metal stocks led the gains. The Nifty Defence index rose by over 3% and the Nifty Metal index increased by around 2.7%. In contrast, there was modest profit-taking in PSU banks, IT and pharma stocks, with the Nifty PSU Bank index slipping close to 1%, and the Nifty IT and Nifty Pharma indices easing by around 0.3%.

NIFTY’s market breadth remained subdued this week, with the percentage of NIFTY50 stocks trading above their 50-day moving average (DMA) remaining in the 45–50% range. This suggests that participation remained limited, even though the index continued to consolidate at higher levels. The inability of the market breadth indicator to reclaim the 60% mark highlights ongoing internal fatigue. This suggests that only a few heavyweight stocks are supporting the index. While this does not signal an outright breakdown, it does suggest a cautious undertone, whereby upside momentum is likely to remain limited unless broader participation improves.

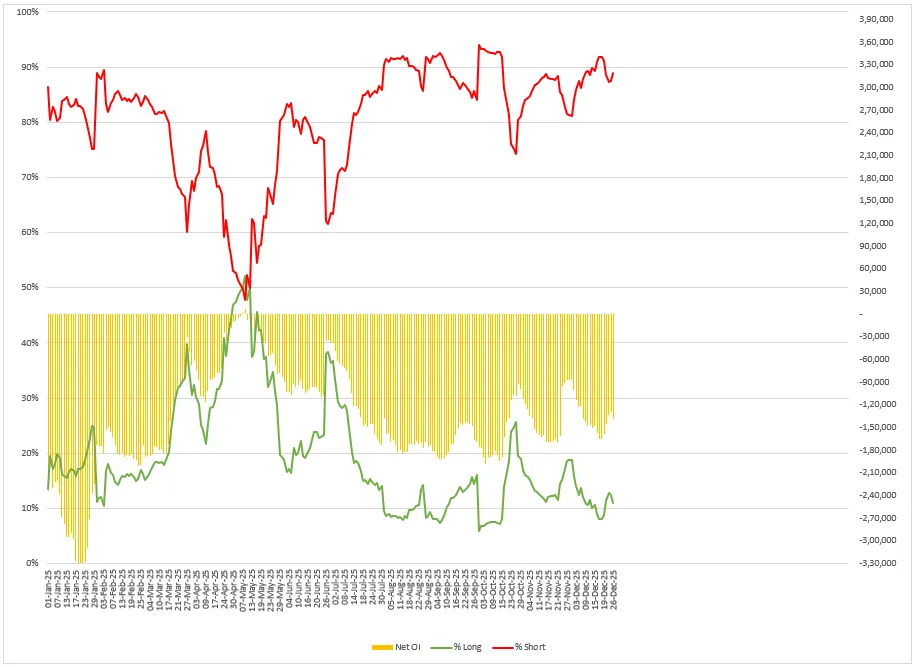

Foreign institutional investors (FIIs) maintained a bearish outlook on index futures, with short contracts accounting for almost 90% of total positions. This highlights continued caution, as FIIs prefer to hedge rather than make aggressive bullish bets. Net open interest also remained deeply negative, suggesting that FIIs are exploiting market strength to offload equities at higher levels. Overall, this positioning is consistent with NIFTY’s ongoing consolidation, suggesting that FIIs are waiting for a clear trigger before changing their approach.

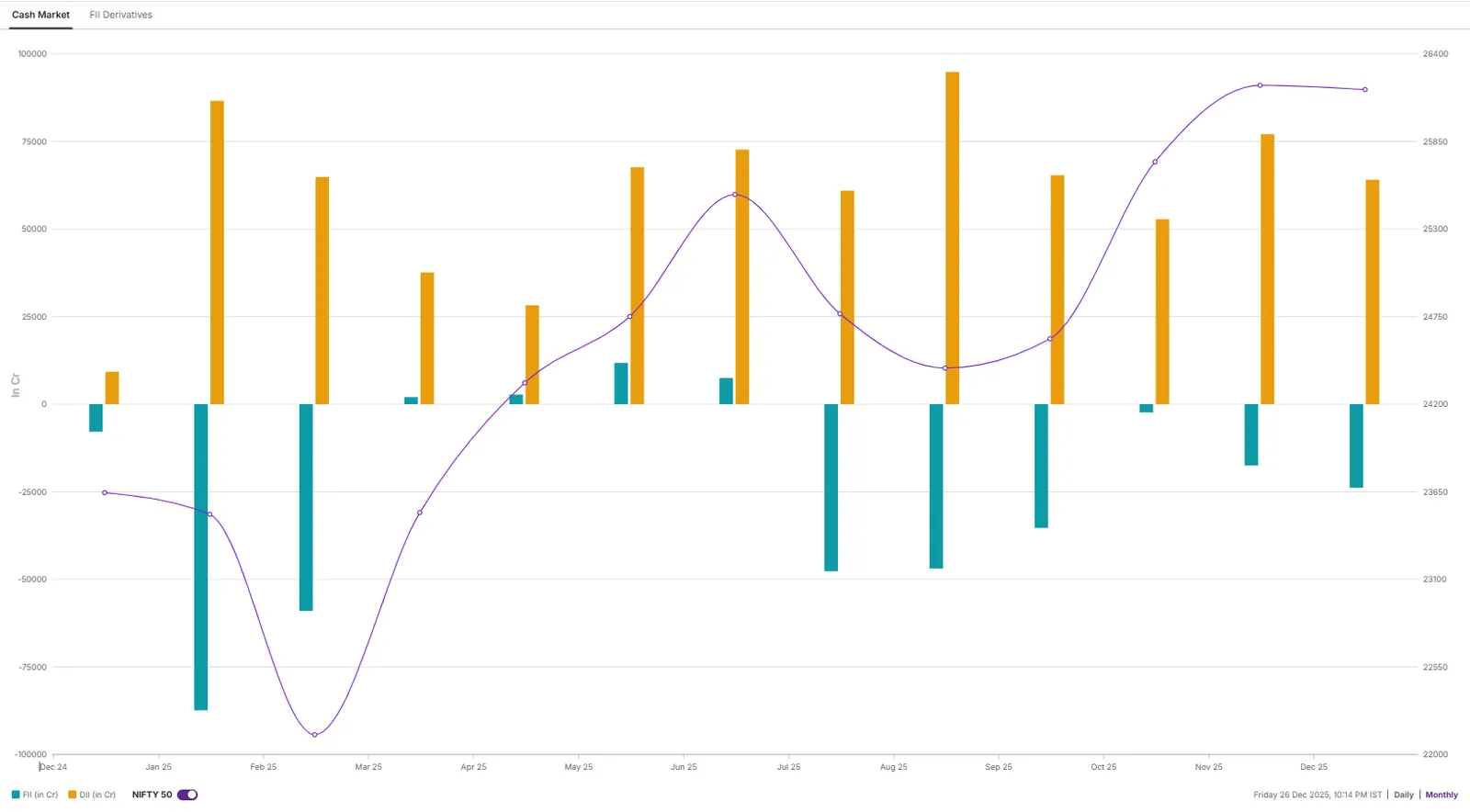

Meanwhile, in the cash market, FIIs have sold shares worth ₹23,830 crore so far in December, marking their highest monthly selling since September 2025. On a year-to-date basis, foreign investors have offloaded equities worth ₹2.9 lakh crore, reflecting a persistently cautious stance on Indian equities. In contrast, domestic institutional investors (DIIs) have continued to provide strong support, buying shares worth ₹64,000 crore in December and ₹7.72 lakh crore for the year so far. This sharp divergence highlights that while foreign investors remain bearish, domestic flows are acting as the key stabilising force for the market.

The NIFTY50 index spent the week consolidating near the 26,000 zone, once again failing to sustain moves toward the upper end of the range. The index faced selling pressure near 26,250, reinforcing this area as a strong resistance, while declines continued to find support around the 25,700–25,750 zone, which coincides with the rising 50-day EMA.

Price action remained choppy, highlighting indecision and lack of follow-through from both buyers and sellers. Despite the short-term consolidation, the broader structure remains positive as NIFTY continues to trade above its key moving averages. A sustained breakout above 26,250 is needed to revive momentum, while a breakdown below 25,700 could invite short-term pressure.

📌Spotlight: The NIFTY Metal index remained a pocket of strength this week, advancing about 2.7% and outperforming the headline benchmarks.. The positive sentiment was helped by expectations of easier global monetary policy in 2026, a softer dollar, which collectively lifted risk appetite for ferrous and non-ferrous names. Within the basket, stocks such as Hindustan Copper (+22%), Hindustan Zinc (+8%), National Aluminium (+10%), Vedanta (+3%) and Steel Authority of India (+5%) were among the notable outperformers, aided by higher underlying commodity prices.

🗓️Key events in focus: The key market triggers next week will be liquidity conditions, policy cues and labour market signals from India and the U.S. In India, attention will turn to the Reserve Bank of India’s (RBI) ongoing government bond purchases and USD/INR swap operations, which are part of its broader plan to inject liquidity into the economy. The impact of these measures on bond yields, system liquidity and risk appetite will be closely monitored, particularly in rate-sensitive sectors.

In the United States, the latest meeting minutes from the Federal Reserve will be a key global indicator, as investors seek clarity on the timing and pace of potential rate cuts in 2026. Alongside this, weekly jobless claims will provide an up-to-date picture of the U.S. labour market. Any signs of weakness could strengthen expectations of a softer growth outlook and increase the likelihood of earlier or more substantial policy easing.

🛢️Crude oil: Crude oil prices remained volatile but ended the week on a weak note, as brief support from geopolitical tensions was outweighed by concerns over ample global supply and rising inventories, keeping pressure on prices as markets look ahead to 2026. Brent crude hovered in the low-$60s and WTI around the mid- to high-$50s, with prices slipping more than 2% on Friday amid renewed optimism over Ukraine peace talks and worries that a resolution could lead to more Russian barrels returning to global markets.

📓✏️Takeaway: Following the reversal price action that has occurred over the past two weeks, NIFTY50 index is clearly signalling a short-term consolidation phase. The broader view remains unchanged, with the index remaining within a defined range and lacking a decisive trigger. Unless NIFTY breaks below 25,700 or moves decisively above 26,250, the market is likely to continue moving sideways, favouring stock-specific opportunities over directional index trades.

Derivatives trading must be done only by traders who fully understand the risks associated with them and strictly apply risk mechanisms like stop-losses. The information is only for consumption by the client, and such material should not be redistributed. We do not recommend any particular stock, securities, or trading strategies. The securities quoted are exemplary and not recommendatory. The stock names mentioned in this article are purely to show how to do analysis. Make your own decision before investing.